10. April 2026

Mezzanine Finance in CRE: Navigating Complexity and Intercreditor Dynamics

In an increasingly capital-constrained commercial real estate (CRE) market, mezzanine finance has become more than a supplementary funding tool: it is now a core structuring mechanism for acquisitions, leveraged buyouts and large-scale redevelopment projects. Yet its value lies not simply in bridging funding gaps, but in how effectively legal and commercial risk is allocated across the capital stack.

In practice, mezzanine finance is rarely about headline pricing alone. Its true significance lies in control, timing and downside protection. The success of a mezzanine structure depends not just on capital availability, but on whether the legal framework is robust enough to preserve value when a transaction comes under stress. The critical question is whether the mezzanine layer is structured to remain in the deal when stress emerges.

Bridging the Capital Gap: Where Mezzanine Sits

Mezzanine finance occupies the layer between senior debt and sponsor equity in the capital stack. In most development transactions, the “sponsor” is the developer or lead project promoter, the party driving the acquisition, securing planning, overseeing construction and ultimately seeking to deliver the project exit.

A typical development capital stack looks as follows:

- Senior debt: 50-65% loan-to-cost (LTC), subject to project gross development value (GDV) and exit loan-to-value (LTV) constraints

- Mezzanine debt: 15-25%

- Sponsor / investor equity: balance

This structure allows developers to reduce the amount of expensive equity required at the outset, while the senior lender's exposure stays within its typical 50-65% LTC range.

Unlike senior debt, which is secured by a first-ranking legal charge over the underlying property and project cash flows, mezzanine debt is more commonly structured either through:

- a second-ranking charge over the property (where commercially acceptable); or

- more typically, a charge over the shares in the special purpose vehicle (SPV) that owns the asset.

The SPV structure is central to the transaction. In most development transactions, the sponsor (developer) establishes a ring-fenced SPV to hold the site, planning rights, construction contracts and project cash flows. By taking security over the shares in that SPV, the mezzanine lender can, in principle, step into ownership of the project entity and take control without requiring a full insolvency process.

This is often described as a “cleaner” enforcement route. However, the effectiveness of that route depends entirely on the intercreditor framework agreed at the outset.

In practice, the senior lender defines the structural envelope of the transaction, including leverage, security and covenant framework. The mezzanine lender then negotiates within that envelope. The intercreditor agreement then decides control, enforcement and the payment waterfall.

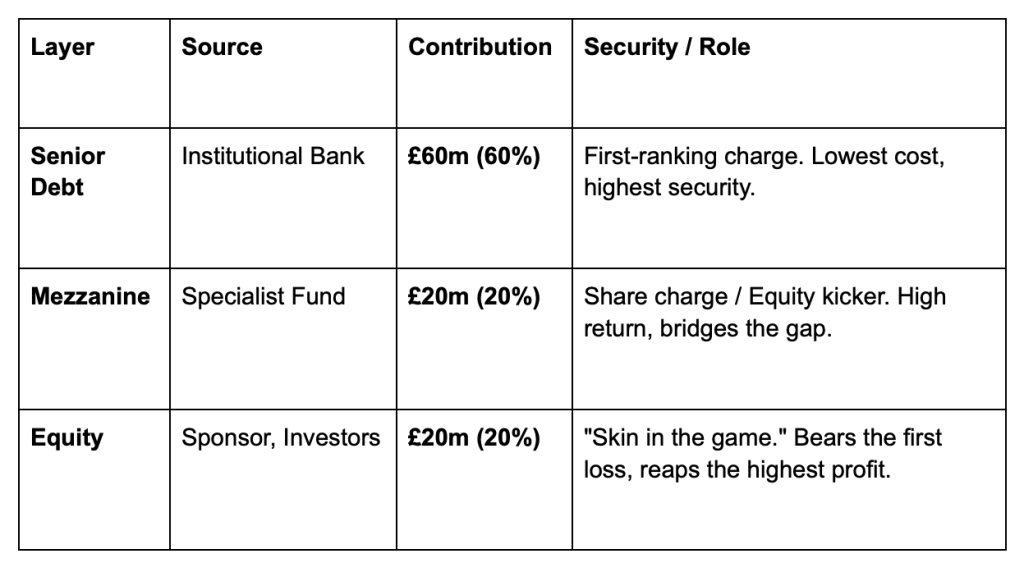

A £100 Million Development: How the Structure Works in Practice

Consider a developer seeking to acquire and redevelop an office asset with a total project cost of £100m.

A typical capital structure would include:

- £60m senior facility (60% LTC)

- £20m mezzanine facility

- £15m investor equity

- £5m developer / sponsor equity.

This structure allows the developer to control a £100m project with a relatively limited equity contribution of £5m.

Transaction Lifecycle

Phase 1: Term Sheets and Structuring

The senior lender typically leads initial structuring by setting:

- pricing;

- drawdown mechanics;

- security package; and

- covenant framework.

The mezzanine lender enters once the senior envelope is known.

At this stage, the intercreditor agreement (ICA) becomes the key negotiation point.

Phase 2: Documentation and Conditions Precedent

Core documents usually include the senior facility agreement, ICA, security package and share charge over the SPV.

Before first drawdown:

- planning approvals must be in place;

- construction contracts agreed;

- insurance arranged; and

- title and security perfected.

Funding is then usually advanced in staged tranches linked to construction milestones.

Phase 3: Exit and Waterfall

Assume the redeveloped office asset is sold two years later for £125m.

Illustrative repayment waterfall is as follows:

- Senior lender: £60m principal + interest / fees ≈ £63m

- Mezzanine lender: £20m principal + interest / fees ≈ £23.5m

- Equity investors: £15m capital + preferred return

- Developer / sponsor: residual upside

This illustrates mezzanine finance’s commercial purpose: enabling projects to proceed without requiring the sponsor to over-capitalise the deal with pure equity. It also highlights a harder truth: mezzanine enhances returns only where the project remains on a credible path to its underwritten exit value.

While the capital stack appears straightforward on paper, its resilience is ultimately determined by the intercreditor framework governing it.

The Real Battleground: Intercreditor Dynamics

The intercreditor agreement is the most strategically important document in any layered financing structure.

In a well-performing scenario, the ICA is largely invisible. In a distressed scenario, it becomes the transaction.

While senior lenders and mezzanine lenders are both aligned in wanting the project to succeed, their incentives diverge sharply when the project underperforms:

- senior lenders prioritise capital preservation and downside control.

- mezzanine lenders, pricing for subordinated risk, seek greater flexibility and intervention rights.

That tension is the defining feature of distressed CRE financings.

Mezzanine pricing reflects its subordinated position and higher risk, and therefore typically sits above senior debt margins linked to SONIA (Sterling Overnight Index Average, the UK's primary overnight interest rate benchmark). This pricing differential is not purely economic: it shapes the negotiation of key intercreditor protections, including standstill periods, cure rights, enforcement control, payment restrictions and debt purchase rights. These are considered below.

1. Standstill Provisions

Standstill provisions restrict the mezzanine lender’s ability to enforce following a default, usually for 90 to 180 days depending on asset profile and transaction complexity. During this period, the mezzanine lender is generally prevented from enforcing its share charge, appointing receivers, accelerating debt or commencing insolvency proceedings.

The rationale is straightforward: the senior lender, as first-ranking creditor with the largest exposure, wants the first opportunity to stabilise the position. In practice, this may involve covenant waivers, restructuring milestones, appointing asset managers or pursuing an orderly sale.

For mezzanine lenders, however, standstill creates immediate risk: value can continue to deteriorate while they are contractually prevented from acting. The legal challenge is therefore balancing senior lender control without rendering mezzanine capital economically trapped.

2. Cure Rights

Cure rights are among the most important protections available to mezzanine lenders. These rights may allow the mezzanine lender to remedy defaults under the senior facility, such as missed interest payments, covenant breaches or insurance failures.

In practice, cure rights serve two critical functions: they reduce the risk of value-destructive acceleration and preserve project optionality while the market stabilises.

For example, where a project experiences a short-term liquidity shortfall due to leasing delays, a mezzanine lender may elect to fund the senior shortfall rather than allow the structure to collapse prematurely.

The legal nuance lies in defining cure periods, notice mechanics, repeat cure limitations and whether cure rights extend to non-monetary defaults. In distressed markets, these rights can make the difference between recovery and structural wipeout.

3. Payment Blockage and Enforcement Control

Mezzanine lenders are typically restricted from receiving payments while the senior facility is in default. These restrictions preserve senior lender priority and prevent leakage from the structure.

Typical restrictions include:

- prohibition on mezzanine interest payments during senior defaults;

- cash sweep triggers; and

- turnover obligations requiring wrongly received payments to be redirected to the senior lender.

This is where legal drafting becomes commercially sensitive: mezzanine lenders require yield, but senior lenders require certainty that subordinate distributions do not impair senior recoverability.

Equally important is the practical enforceability of mezzanine security. Share charge security may appear attractive on paper, but practical control depends on whether the SPV is genuinely ring-fenced, whether key project contracts are assignable, whether replacement directors can be appointed quickly, and whether enforcement triggers are objectively drafted.

4. Debt Purchase and Uplift Rights

The most significant tool available to a mezzanine lender is often the contractual right to purchase the senior debt following a default. Under standard ICA mechanics, upon a senior loan event of default, the mezzanine lender may exercise a purchase option, acquiring the senior lender's entire position at par plus accrued interest and enforcement costs. Once exercised, the mezzanine lender steps into the senior lender's shoes, becoming the first-ranking creditor with control over enforcement timing and any restructuring process. This "uplift" transforms the mezzanine lender from a subordinated creditor into the controlling party of the entire capital stack. For senior lenders, the risk is strategic: a mezzanine lender with purchase rights can dictate the terms of any workout. For mezzanine lenders, preserving robust purchase rights without artificially truncated time limits is among the most valuable protections in any ICA.

Debt purchase rights are powerful, but they are only as valuable as the mezzanine lender's ability to exercise them before value deteriorates. The following case study illustrates the consequence of structural weakness.

A Case Study in Mezzanine Risk: 5 Churchill Place

5 Churchill Place is one of the clearest examples of capital stack mechanics in distress.

Originally acquired in 2017 by Cheung Kei Group for approximately £270 million, the building was financed through:

- senior debt from Lloyds Bank; and

- mezzanine debt from Hanwha Asset Management.

What followed was not a single failure, but a convergence of factors: weakening post-COVID office demand, increasing pressure to refinance, declining asset values and constrained exit options. As debt accrued and market liquidity weakened, the project became structurally impaired.

The asset was ultimately sold for around £110 million, approximately 60% below the original acquisition price. Senior lender recoveries dominated sale proceeds, rendering the mezzanine position effectively wiped out.

This is the mechanical reality of subordinated debt: when exit assumptions fail, mezzanine absorbs losses before equity can preserve upside.

In mezzanine finance, it is legal optionality that ultimately matters. A well-structured ICA may provide mezzanine lenders with tools to mitigate downside, including cure rights, debt purchase options, step-in rights and share charge enforcement.

But these protections only matter if they are commercially realistic and exercisable before value has already deteriorated.

When Mezzanine Works: The Carlyle (Uncommon Refinancing)

A more recent transaction showcases how mezzanine finance can function effectively when aligned with asset performance and capital structure discipline.

In October 2024, The Carlyle Group refinanced a portfolio of five central London office assets operated under its “Uncommon” brand. The transaction comprised a £120 million senior facility from Société Générale and a £35 million mezzanine facility from Deva Capital. DLA Piper advised Carlyle while the senior and mezzanine lenders were separately represented.

In this context, the mezzanine layer served its intended purpose. It enabled the sponsor to access additional leverage without diluting control, while maintaining a capital structure acceptable to the senior lender from a risk perspective.

Crucially, the underlying assets remained on a credible path to stabilisation and value realisation. This allowed the mezzanine lender to price for risk without relying on enforcement-driven outcomes.

The refinancing completed in Q4 2024, with all facilities fully drawn and the portfolio continuing to trade in line with underwriting assumptions. The transaction demonstrates that where asset fundamentals, timing and capital structure are aligned, mezzanine finance operates not as a source of structural tension, but as a mechanism for efficient capital deployment.

While the Carlyle refinancing proves that mezzanine can unlock efficiency, and 5 Churchill Place illustrates the downside of fragmented control, large-scale self-funded developments such as JPMorgan’s planned £3bn Riverside South headquarters at Canary Wharf (as at April 2026) demonstrate the opposite dynamic: where capital is not layered, control remains unified. In contrast, mezzanine structures introduce multiple decision-makers, and it is within that fragmentation that value is either preserved or lost.

What Matters in Practice

For developers, lenders and advisors structuring layered transactions, the key considerations are therefore:

- aligning debt maturity with the point at which the project can realistically generate liquidity, whether through sale, refinancing or stabilised income;

- stress-testing downside enforcement scenarios;

- drafting payment waterfalls with precision;

- ensuring cure and step-in rights are genuinely exercisable; and

- preserving value before distress becomes irreversible.

The ASGV Legal Perspective

In layered CRE transactions, risk rarely sits in the headline term sheet. More often, it arises in the gaps between legal rights, commercial expectations and timing under pressure.

Effective mezzanine structuring begins before the documents are signed. It requires anticipating where friction will arise and allocating control before that friction materialises.

At ASGV Legal, we advise sponsors, lenders and investors on structuring transactions that are not only legally robust, but commercially resilient, ensuring capital stacks work in practice, not just on paper.

This article is for general information only and does not constitute legal advice.